Maximising Business Relief allowances for spouses

About this scenario

This scenario outlines how advisers can help married clients make the most of the new Business Relief allowance for inheritance tax (IHT) planning from 6 April 2026, to achieve faster inheritance tax relief, retain access to capital, and support efficient wealth transfer.

We created this tax planning scenario to help advisers develop suitable planning strategies for clients. It does not provide advice on investments, taxation, legal matters, or anything else. As you know, tax-efficient investments aren’t suitable for everyone.

Any recommendation should be based on a holistic review of a client’s financial situation, objectives and needs. Before recommending an investment, you should also consider the impact of charges related to the product, such as initial fees, ongoing fees, and annual management charges.

Meet Carol and Jim who want to maximise their allowances

Carol and Jim are in their seventies with a combined estate of £6 million held equally and jointly, mainly in listed shares, pensions and property. Their adviser explains that due to the size of their estate they would be subject to a large inheritance tax liability.

They wish to reduce the IHT liability their children will face on their estate, by maximising their shareable IHT allowances, while retaining access to the capital should they need it. Given their age, they would like a strategy that can attract IHT relief quickly.

Their adviser explains that from 6 April 2026, a £2.5 million Business Relief allowance applies to qualifying agricultural property and unquoted business assets (private company shares, partnership interests and sole traders). Amounts within this allowance attract 100% relief from inheritance tax and amounts above this allowance will attract relief at 50%. The allowance importantly is transferable between spouses, similar to the transferable nil rate band (NRB) and residence nil rate band (RNRB), where on first death the spouse hasn’t used their full allowance.

An estate planning solution

Their adviser assesses their needs, objectives and appetite for risk and recommends redirecting £1.5 million worth of their assets into an unquoted Business Relief portfolio, such as the Octopus Inheritance Tax Service (OITS) to achieve their objectives:

Fast inheritance tax relief:

Business Relief investments qualify for IHT relief in just two years, which is significantly shorter than other IHT strategies, such as the seven-year gifting period.

Frees up the NRB and RNRB:

Importantly, BR qualifying assets do not use up other IHT allowances like the NRB or the RNRB, unlike other assets.

Retain access to capital:

With a Business Relief investment, the investment will be in their name should they wish to access.

How it works in practice

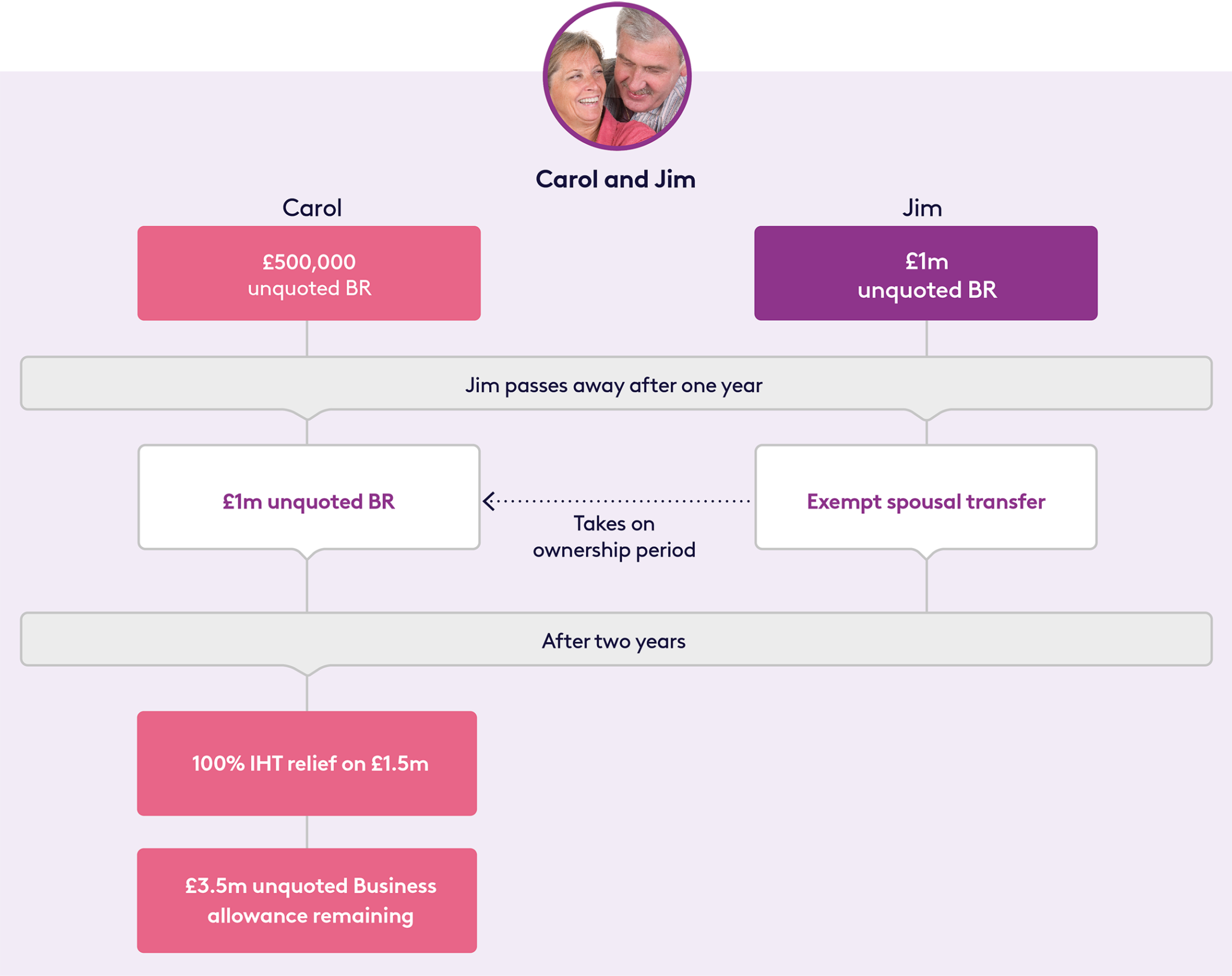

Carol and Jim’s adviser recommends they invest separately with £1 million for Jim and £500,000 for Carol as this gives them flexibility of how and who the assets are passed to on death.

After holding the shares for one year, Jim passes away. In his Will, he directs his unquoted Business Relief portfolio to Carol as he has held the shares for less than the required two year holding period. Carol takes on the Business Relief ownership period of Jim’s shares as a result of the transfer, which means she needs to hold his shares for one more year to qualify for IHT relief.

After two years since their initial investment, Carol now has £1.5m of unquoted Business relief, which should attract 100% relief from IHT. She also has £3.5 million of unquoted Business Relief allowance left, which she can invest further for 100% IHT relief.

This is because she has taken on £2.5m of Jim’s allowance, which he did not use, and has her own allowance of £2.5m.

This approach allows Carol and Jim to maximise their Business Relief allowances, retain access to some capital, keep control over how their wealth is distributed, and efficiently pass on up to £5 million free from inheritance tax.

Notes and assumptions:

- Tax rates and allowances are correct for the tax year 6 April 2026 to 5 April 2027.

- From 6 April 2026, a £2.5 million Business Relief (BR) allowance was introduced for qualifying agricultural property and unquoted business assets. Amounts up to this allowance receive 100% relief from inheritance tax. Qualifying investments above this allowance attract relief at 50% (as do all qualifying AIM-listed shares). Before 6 April 2026, BR applied without any cap to all qualifying investments. For more information, visit the HMRC website and search for ‘Business Relief’

- For ease of comparison, we’ve assumed no gains or losses on the assets referenced, and no product fees or charges paid for financial advice have been included which may apply.

Risks to bear in mind

Capital at risk

BR-qualifying investments are high-risk. The value of an investment, and any income from it, can fall as well as rise. Investors may not get back the full amount they invest.

Tax treatment may change

Tax treatment depends on individual circumstances and tax rules could change in the future.

The investment may be volatile and difficult to sell

The shares of unquoted companies could fall or rise in value more than shares listed on the main market of the London Stock Exchange. They may also be harder to sell.

BR is assessed on a case-by-case basis

Tax relief depends on portfolio companies maintaining their qualifying status.

More tax planning scenarios?

Estate planning for clients who’ve sold a business in the last three years

Alan recently sold his business and wants to leave the proceeds to his daughters free of inheritance tax.

Estate planning for clients who want to retain access to capital

Carol is aged 86 with a large estate. She's worried about unexpected care costs and is reluctant to gift.

Estate planning for clients who worry it’s too late

Harold worries that in his 90s it's too late to plan for inheritance tax.

Estate planning for clients who want to settle assets into trust

Louise is worried that her child's marriage will end in divorce, and wants control over what will happen to her assets.

Estate planning for clients who want an inheritance tax-efficient ISA

Peter has a large ISA pot that's subject to inheritance tax. He wants to plan for inheritance tax but keep the benefits of the ISA wrapper.