Estate planning for clients who have inherited a spouse’s ISA

Estate planning

What to do for clients who have inherited a spouse’s ISA?

An Individual Savings Account (ISA) offers valuable tax benefits during someone’s lifetime, but is still subject to inheritance tax along with the rest of the person’s estate.

This example explains how clients who have inherited a spouse’s ISA can use Additional Permitted Subscription rules as part of their estate planning.

Remember, Business Relief won’t be right for everyone. It puts investor capital at risk and comes with other considerations. We cover the risks in more detail in this scenario.

About this planning scenario

This is a tax-planning scenario designed to help you build appropriate strategies for your clients.

Nothing here should be viewed as advice. Any suitability decisions should be based on a client’s objectives and needs, as well as their attitude and capacity for risk.

Advisers should consider the value of tax reliefs for a client and the impact of charges relevant to the product represented or any product chosen.

Meet Sylvia

Meet Sylvia, who recently lost her husband Gordon

Sylvia is sorting out Gordon’s estate. He left all his assets to her, including his Stocks and Shares ISA worth £200,000.

Sylvia’s estate is above the usual inheritance tax allowances and faces a sizeable inheritance tax liability when she dies. Gordon’s passing has encouraged her to look at how she can pass on as much to her three children as possible.

A tax-planning solution

Sylvia’s financial adviser explains that due to the APS rules, Sylvia has the opportunity to reinvest some or all of the value of Gordon’s ISA into a new ISA of her choosing. If she does so she will benefit from the lifetime tax benefits such as tax-free interest, dividends, and growth that an ISA wrapper affords.

A new ISA taken out by Sylvia will be subject to inheritance tax when she passes away. At 40%, that would mean an inheritance tax bill of £80,000 on the ISA pot alone.

Sylvia’s adviser makes an assessment based on her circumstances and her objectives, including the fact that she doesn’t need to access the amount she inherited from Gordon, and the fact that she is keen for that money to stay invested in stocks and shares which has the potential to grow for her children.

Sylvia’s adviser suggests she opens an Octopus AIM Inheritance Tax ISA that is specifically managed to invest into companies that qualify for Business Relief (BR). As long as she has held the investment for at least two years when she dies, it will pass to her children free from inheritance tax. It’s worth remembering that ISAs which invest in AIM-listed companies and those which qualify for BR are likely to have a higher risk profile than standard stocks and shares ISAs.

Key risks

Sylvia’s adviser explains the risks

Sylvia’s adviser makes it clear that the value of a BR qualifying investment, and any income from it, can fall as well as rise. She may not get back the full amount she invests.

He also explains that BR is assessed by HMRC on a case-by-case basis, and that this assessment happens when an estate makes a claim. The ability to claim the relief will depend on the company or companies Sylvia invests in qualifying for BR at the time the claim is made.

Tax treatment will also depend on her personal circumstances, and tax legislation could change in the future.

Her adviser makes it clear that withdrawals cannot be guaranteed, as the shares of unquoted and AIM-listed companies can be harder to sell than shares listed on the main market of the London Stock Exchange. Their share price may also be more volatile.

Get in touch with your local IHT expert to discuss this scenario

How it works

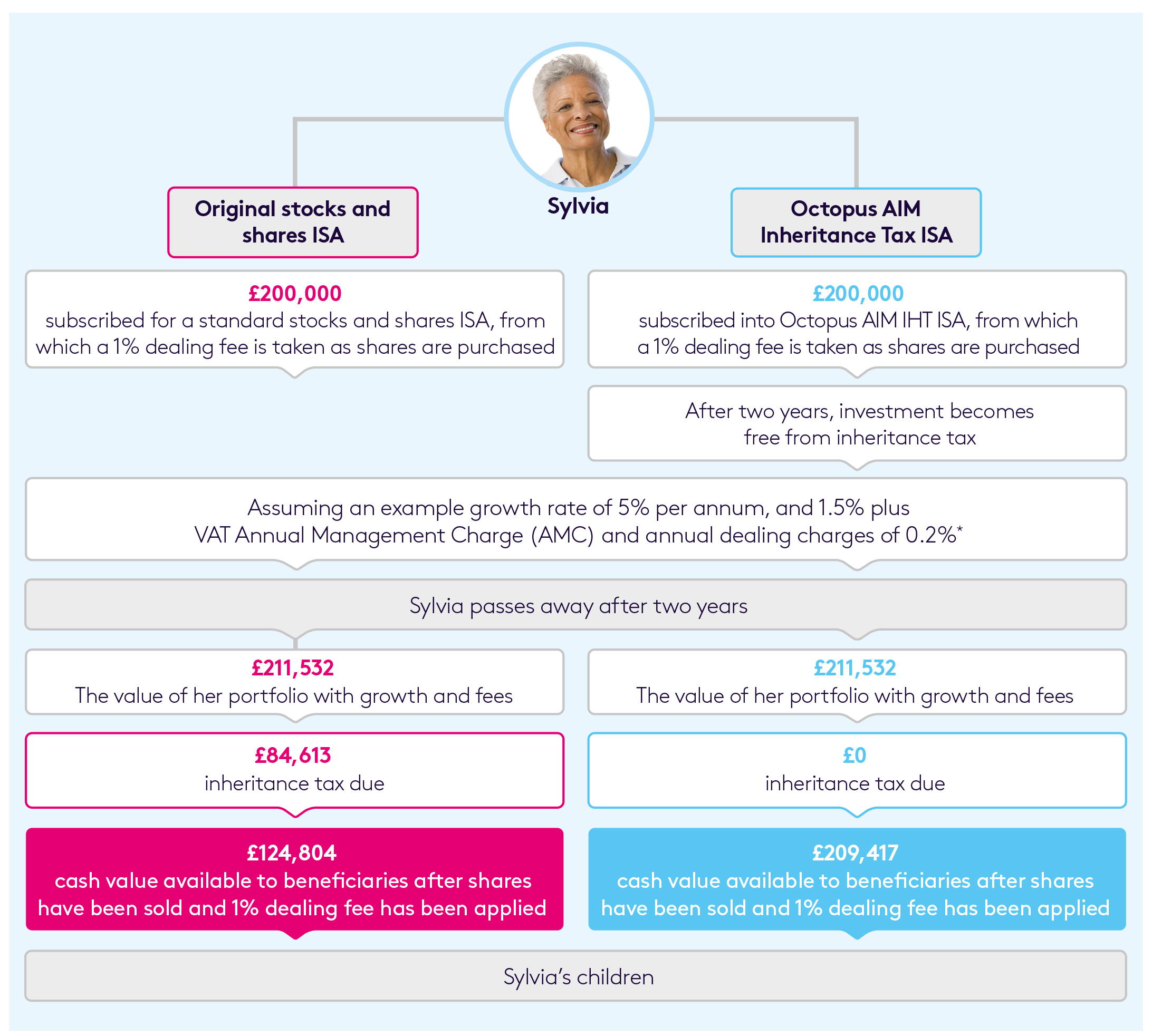

How it works in practice

Let’s see how it might look if Sylvia were to invest in the Octopus AIM Inheritance Tax ISA, a service that invests in the shares of one or more AIM-listed companies expected to qualify for BR.

Please note:

- This example is for illustration purposes only and assumes that the nil rate band is offset against other assets. It is important to note that the risk profile of each portfolio, and any investment growth or losses, is likely to differ. Investments in AIM-listed companies can fall or rise in value much more sharply than shares in larger, more established companies.

- *The annual management charge is 1.5% +VAT. The estimated annual dealing charges are 0.20%, typical for the Octopus AIM Inheritance Tax ISA. However, actual dealing charges experienced by an investor may be higher or lower.

- The example assumes the costs for each portfolio are the same, but actual costs may be different. It does not include any charges paid for financial advice.

Find out more about how the Octopus Inheritance Tax Service could help clients like Sylvia

Other scenarios