Extracting money from a business

It may be advantageous for small business owners to take out surplus money that’s building up in their business. Changes to dividend taxation mean small business owners and entrepreneurs who pay themselves through dividends could face higher tax bills and lower take-home earnings.

This tax-planning scenario explains how clients can use a Venture Capital Trust (VCT) to extract surplus money from a business.

Build appropriate strategies for your clients

This scenario might be useful for clients who:

- Want to reduce their income tax bill.

- Are looking for tax-efficient ways make a withdrawal from their business.

Things to keep in mind

- Nothing in this scenario should be viewed as advice.

- Any suitability decisions should be based on a client’s objectives and needs, as well as their attitude and capacity for risk.

- You should consider the value, eligibility and timings of tax reliefs and liabilities.

- You should consider the impact of relevant product charges (including initial and ongoing) like administration fees and annual management charges.

Vijay wants to make a tax-efficient extraction from his small business

Vijay is an independent IT contractor. Because he works as a consultant for a number of different companies, he has established a limited company.

Vijay chooses to pay himself a combination of a salary of £12,570 (within his National Insurance Contribution threshold) and a dividend of £37,700. He owes £3,255 in tax, meaning after tax, he’ll be left with £47,015 in available cash.

Vijay also pays into his pension and chooses to invest in some new technology for his business. But he’s still left with surplus money building up in his business. There’s an opportunity cost to not better utilising this money, but there may also be other tax implications in the future if it continues to build.

Because of this, Vijay is keen to extract an additional dividend from his company but is wary about the extra tax he would owe.

Vijay’s financial adviser suggests investing in a VCT

Vijay talks to his financial adviser, who makes an assessment based on:

- His risk profile.

- His investment time horizon: more than five years.

- His attitude towards investing in smaller companies.

Given Vijay’s goal of extracting surplus money tax efficiently, his adviser suggests that he pay himself an additional £50,000 dividend and invest it into a VCT, holding the investment for at least five years.

With a VCT, Vijay can claim up to 20% income tax relief on up to £200,000 invested in any single tax year – provided he holds his VCT shares for at least five years. Vijay can also benefit from tax-free dividends and no capital gains tax to pay when he sells the shares.

Risks to remember when investing in a VCT

- VCTs are high risk and should be considered as long-term investments. The value of an investment, and any income from it, can fall or rise. Investors may not get back the full amount they invest.

- Tax treatment depends on individual circumstances and can change in the future. Tax reliefs also depend on the VCTs maintaining its qualifying status. Tax relief is available on investments of up to £200,000 per year.

- VCT shares could fall or rise in value more than other shares listed on the main market of the London Stock Exchange. They may also be harder to sell.

An overview of VCTs

VCTs were first introduced in 1995 and they’ve grown in popularity since. They’re a good fit for investors who:

- Already have personal pensions and Individual Savings Accounts (ISAs).

- Are comfortable with higher risk investments.

VCTs have a different risk profile to pensions and ISAs and shouldn’t be compared on tax reliefs alone. A VCT isn’t likely to be suitable for investors who:

- Need guaranteed income.

- Can’t tolerate loss.

- Want to keep immediate access to their money.

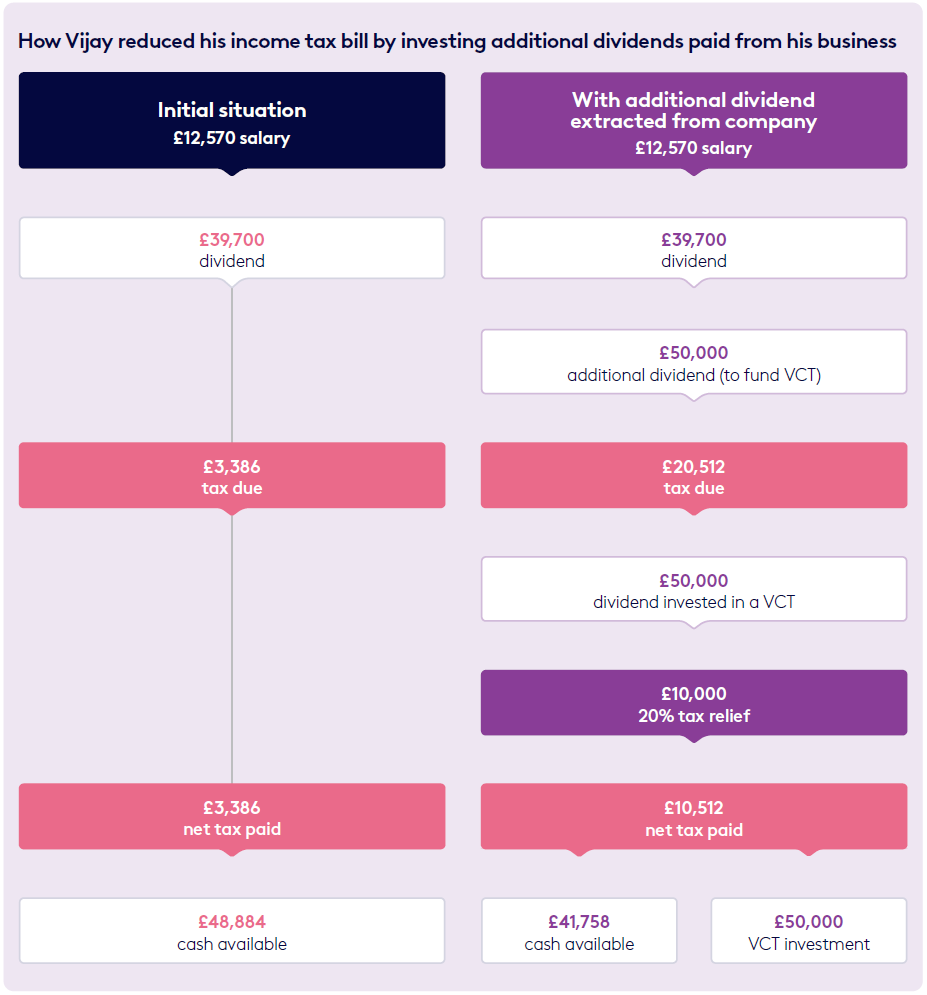

Tax benefits of investing dividends in a VCT

This diagram shows how a small business owner can take advantage of the tax benefits associated with investing in a VCT to offset some of their dividend tax bill. VCTs are high risk and if an investor needs guaranteed income, cannot tolerate loss or is uncomfortable losing immediate access to their money, then a VCT will not be suitable. Clearly everyone’s circumstances are different, and VCTs won’t be suitable for all, but the attractive tax benefits mean that VCTs could be considered as part of a portfolio for some people.

Please note that before investing in a VCT, investors should read the product prospectus and Key Information Documents (KID).

Tax rates and allowances are correct for the tax year 6 April 2026 – 5 April 2027. For purposes of this illustrative example, we have assumed no gain or loss on investments, and it does not take into account any initial fees or ongoing charges that will be incurred. VCTs are high risk and inherently different from pensions and ISAs.

When clients choose to sell VCT shares, they are often sold at a small discount to the value of their underlying net asset value, so the impact of this should also be considered when assessing any specific products. Please note, after selling shares in a VCT, it is not possible to claim tax relief on new shares bought in the same VCT within six months of the initial sale.

Interested in VCTs?

We’re the largest provider of VCTs in the market, offering three types of

investments that can provide attractive tax reliefs.

Octopus AIM VCTs

closed

Two VCTs featuring established portfolios of around 80 AIM-listed companies with growth potential.

Octopus Apollo VCT

closed

A portfolio of around 45 established smaller companies which targets commercialised businesses looking to scale.

Octopus Titan VCT

closed

The UK’s largest VCT invests in a portfolio of over 140 early-stage companies with the potential for high growth.

About Octopus

We’re a financial services provider with a difference. Our main goal is to help people plan for their financial future, so we’ve built market-leading positions in tax-efficient investment, smaller company financing, renewable energy and healthcare.

Related VCT resources

Venture Capital Trusts Explained

Learn how VCTs function, the types of early-stage companies they invest in, and the tax benefits and risks involved.

How to claim VCT tax relief

Learn how to claim up to 20% income tax relief on Venture Capital Trust (VCT) investments and enhance your understanding to support your clients’ investment decisions.

VCT FAQs

Our easy-to-read guide answers common questions about Venture Capital Trusts (VCTs), designed to help you understand VCTs better and assist your clients with confidence.