For equities, 2022 was a challenging year. Economic and geopolitical concerns buffeted markets and our funds weren’t immune.

This uncertainty triggered a significant de-rating of growth equities. But, in our view, it also triggered one of the best buying opportunities in over a decade.

Drivers of the sell off

Ten years of quantitative easing. The Financial Crisis of 2008. Covid pandemic super-stimulus. Supply chain disruption. And then a displaced workforce put central banks on alert last year prompting the initial de-rating of equities.

2022 saw the coming together of a multitude of negative factors to create a ‘perfect storm’ for the bear market.

In February, the market was guilty of underestimating the impact of the war in Ukraine. Food and commodity prices were placed under further pressure, prompting central banks to take a more aggressive stance than had been expected. UK inflation hit 11.1% by October 2022.

The great de-coupling

Our focus on quality-growth, which has a bias toward small and mid-cap growth companies, was a part of the market significantly impacted during the sell-off. However, we believe there remains a lot of opportunity in the UK, as well as a large number of strongly trading businesses – many of which are in the portfolios we manage.

Whilst we haven’t been rewarded with near-term performance, we retain our focus on companies which we believe can grow earnings throughout the economic cycle. We have been largely reassured by the underlying operational performance of many of these growth companies, despite many share prices de-coupling from these solid fundamentals. We are confident that when market conditions normalise, many of these stocks will re-rate significantly, offering investors attractive returns over the medium term.

The last time we encountered share prices deviating from the earnings trajectory of companies to this extent was during the financial crisis, when a significant valuation gap or ‘store of value’ emerged during what became a prolonged ‘risk off’ period. That turned out to be the buying opportunity of the decade. We are currently in that same valuation territory, although calling the market trough is clearly the key near term challenge.

Poised for a rerating?

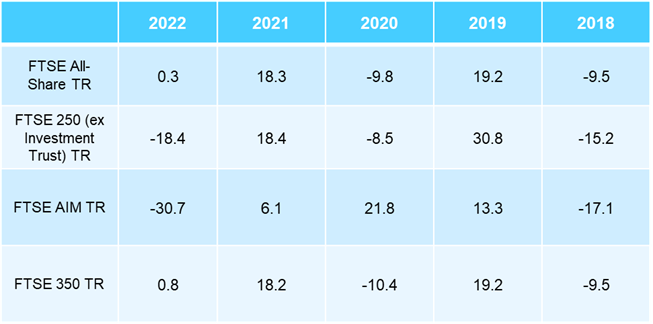

For 2022, the FTSE All-Share ended the year up 0.3%, whilst the more domestically focussed FTSE 250 fell 18.4%, with the FTSE AIM All-Share down 30.5%. The relatively resilient performance of the FTSE All-Share against other benchmarks, was largely a result of its high exposure to commodity stocks and ‘value’ areas of the market, such as tobacco and financials. These sectors performed relatively strongly as the market moved more defensively and rotated away from growth stocks.

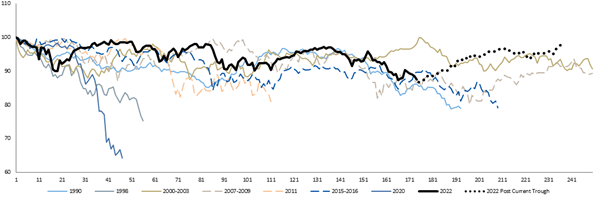

The chart below highlights that, with a start date of 10 February 2022 the FTSE 350 is now almost 240 trading days from its previous peak. If the market did indeed trough back in October, the peak to trough pull back would have lasted 175 days, its fifth longest pull back in the last thirty years. Looking ahead to 2023, while uncertainties remain, multiples are at levels which are clearly attractive.

FTSE 350: Average index declines (peak to trough) in the past downturns rebased to 100

Source: RBC, Datastream

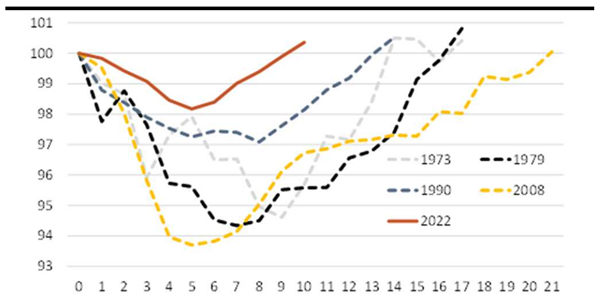

2023: Where are we now?

The chart below looks at the current FTSE 250 consolidated earnings forecasts, and valuation multiples. It highlights the earnings trajectory (red line), index level (white line) and P/E multiple (green line) over the last thirty years.

The consistent growth trajectory of the red line is clear. But focusing on the green line, the FTSE 250 2 year Forward P/E multiple is now at levels which have only been tested a handful of times over the last 30 years.

Whilst earnings across the market have been resilient to date, revisions are now starting to skew to net downgrades, something which is expected to continue into the first half of 2023. However, the chart below shows that in recent cycles, the market starts to recover well ahead of the full extent of estimate revisions.

FTSE 250: Price (White), PE FY2 (Green), EPS FY2 (Red) – 30 years to date

Source: Factset, Octopus

The marker in 2023 will undoubtedly remain driven by macro factors, at least for the first quarter. We would suggest, however, that the market is far more likely to look past the recession, assuming it is indeed modest, and start to look toward recovery as we progress through the year. The market will also remain focused on pivots, particularly around the interest tightening cycle.

Timing the switch from a focus on recessionary risks, to a recovery approach will be key to performance in the year ahead. As we have discussed above, many growth companies are trading at levels that arguably price in earnings cuts, which we would hope would not be realised. We therefore believe these stocks have mid-term value.

The UK is likely already in a recession, as many market commentators have noted. The depth and longevity of this recession is still to be determined. We remain reassured by the relatively resilient trading performance of many growth companies to date, and are believe the UK will face a relatively modest recession compared to previous cycles.

Duration of UK recessions, plus forecasts

Source: Berenberg

Combining this potential economic outcome, with our positioning and current market valuations, it again reinforces our view that current levels present an attractive entry point for UK Equity investors taking a medium-term view.

The promising return of M&A

Finally, we note that mergers and acquisitions activity has started to pick up. This reinforces the view that significant value exists amongst many UK growth companies. During much of 2022, deal activity was quieter than may have been expected given valuation levels, likely because of interest rate volatility. As conditions have normalised, M&A from both corporate and private equity interest has started to resurface with several transactions announced in recent weeks.

Within the last month, we have seen bids for Crestchic by former FTSE 100 stalwart Aggreko, K3 Capital announced that it is being acquired by US private equity firm Sun Coast Capital, and Curtis Banks has seen a bid materialise from Nucleus. We suspect others will follow due to the combination of low valuations and relative Sterling weakness.

Strong underlying performance is key

Cycles are a natural part of stock markets, and investor risk appetite can have a significant impact on share prices in the short term. What remains important is the performance of the underlying companies themselves. These are continuing to grow profits and dividends and are therefore creating value for underlying shareholders. This will be reflected in share prices once market sentiment improves. Whilst we are expecting the current market volatility to remain a feature, at least in the short term, current share prices offer a very attractive entry point for those investors prepared to take a medium-term investment horizon.

At the time of writing, companies referenced within this article are held within Octopus managed funds and discretionary managed portfolios.

Find out more

If you’d like to hear more about the funds or ask us a question directly, please register for an upcoming webinar by clicking on the link below:

Discrete 1-year performance % return to December

Past performance is not a reliable indicator of future results. Source: Lipper to 31/12/22. Returns are based on published dealing prices, single price mid to mid with net income reinvested, net of fees, in sterling.

Risks to bear in mind

The value of an investment can fall or rise and you may not get back the full amount you invest. Smaller company shares are also likely to fall and rise in value more than shares in larger, more established companies listed on the main market of the London Stock Exchange. They may also be harder to sell.

Our investments are not suitable for everyone. We do not offer investment or tax advice. Personal opinions may change and should not be seen as advice or a recommendation. Before investing you should read the Prospectus, the Key Investor Information Document (KIID) and the Supplementary Information Document (SID) as they contain important information regarding the fund, including charges, tax and fund specific risk warnings and will form the basis of any investment. The Prospectus, KIID and application forms are available in English at octopusinvestments.com. The Authorised Corporate Director (ACD) of these funds is FundRock Partners Ltd which is authorised and regulated by the Financial Conduct Authority no. 469278, Registered Office: 8/9 Lovat Lane, London EC3R 8DW. Issued by Octopus Investments Limited, which is authorised and regulated by the Financial Conduct Authority. Registered office: 33 Holborn, London EC1N 2HT. Registered in England and Wales No. 03942880. January 2023. CAM012652.